I (34F) have been managing my mom Rosemary’s (71F) finances for about six months, ever since her second hip surgery left her mostly housebound. She trusted me completely with everything — her accounts, her bills, her pension deposits. I thought I had a handle on things.

Three weeks ago she mentioned, completely casually, that she’d given some money to a man named Gerald who’d been calling her every Tuesday for months. She said he was helping her “secure her retirement.” She said it like she was telling me about a new TV show she liked.

Gerald had taken $47,000.

I went cold in a way I’ve never felt before. Forty-seven thousand dollars. Her entire savings account. Gone in wire transfers over fourteen weeks, each one just small enough that the bank’s fraud alerts never kicked in.

Here’s where it gets complicated.

I pulled the transaction records and something didn’t add up. The wires were authorized in person at her branch — the one on Millbrook Avenue — on days when my mother physically could NOT have been there. She had documented physical therapy appointments. I have the receipts. Someone at that branch processed those transactions without her present.

I called the bank’s fraud line. They opened a “review.” That was two weeks ago. Nothing.

So last Thursday I walked into that branch myself.

I had a folder. Fourteen transaction records, twelve physical therapy receipts, a written timeline, and a printed copy of the bank’s own elder financial abuse policy that they are LEGALLY required to follow.

I asked to speak to the branch manager, a woman named Diane (50s, very pressed blazer, very fake smile). I explained everything calmly. I showed her the documents. I told her someone at this branch had processed fraudulent transactions on a disabled seventy-one-year-old woman’s account.

She told me the transactions were “properly authorized” and that my mother may have “made decisions she later regretted.”

I want you to understand what she said. She looked me in the eye and told me my mother — who can barely walk — CHOSE to drive to the bank fourteen times and hand over her life savings to a con artist. And that was that.

Something in my chest just snapped.

I did not leave. I stood in the middle of that lobby, and I started talking — loud enough for every single person in that room to hear — about exactly what this branch had done to a seventy-one-year-old woman on a fixed income. I named the policy they violated. I named the dollar amount. I named Diane by name.

People stopped. Tellers froze. A man in line actually took out his phone.

Diane told me to lower my voice or she’d call security.

My friends are split. Half of them think I finally did what needed to be done. The other half think I humiliated myself and made it worse for my mom legally.

But here’s the thing they don’t know yet — the thing I found out AFTER I left that lobby.

That man with the phone? He wasn’t a customer.

What I Knew Walking In

I should back up, because the last six months didn’t happen overnight.

When Rosemary’s surgeon told us she’d need a second hip replacement — the first one had gone wrong, some alignment issue I never fully understood — I volunteered to take over her finances before she even asked. She lives forty minutes from me, in the house she and my dad bought in 1987, the one with the aluminum siding she refuses to paint because Dad picked the color. She’s stubborn in ways that are funny until they’re not.

She handed me a shoebox with her account numbers, her pension paperwork, her insurance cards, and a Post-it note with her PIN written in her handwriting from probably fifteen years ago. She trusted me with all of it without blinking.

I set up automatic bill pay. I organized everything into a binder. I checked her balances every Sunday morning with my coffee.

I thought I was doing a good job.

What I wasn’t doing — what I didn’t think to do — was watching for outgoing wires. Her account had never had outgoing wires. Why would it? She’s 71. She buys groceries and pays her utilities and sends birthday checks to my kids.

The first wire went out in October. $3,200. To a holding company in Florida with a name that sounds like a financial planning firm. I found it when I finally pulled the full transaction history, three weeks ago, sitting at my kitchen table at eleven at night while my husband slept.

I counted fourteen of them. The smallest was $2,800. The largest was $5,100. Fourteen weeks, fourteen Tuesdays, like Gerald had a calendar.

$47,000 in total.

I sat there for a while before I did anything. Just sat.

The Receipts

The physical therapy thing — that’s what broke it open.

Rosemary’s PT clinic is on the other side of town from the Millbrook branch. She goes Tuesdays and Thursdays, has since August. Her PT, a guy named Dennis who she calls “very bossy but effective,” keeps meticulous attendance records because insurance requires it.

I called Dennis the morning after I found the wires. Explained what I was looking at. He pulled her file and read me the dates without me asking him to frame it any particular way.

Ten of the fourteen wire transfer dates matched her PT appointment times. Exactly. Rosemary was on a table having her hip worked on while someone at Millbrook Avenue was authorizing five-figure transfers from her account.

The other four Tuesdays? I checked her medical transport records. She uses a service because she can’t drive anymore. Those four Tuesdays, she hadn’t been booked for any transport at all.

So either she walked four miles to the bank and back on a hip that can barely manage the distance from her bedroom to her kitchen, or she didn’t go.

I printed everything. Color-coded the dates with a highlighter. Made three copies of the folder.

One for me. One for the fraud line I’d already called. One for whoever I was going to hand it to at that branch when I walked in there and made them look at it.

Diane

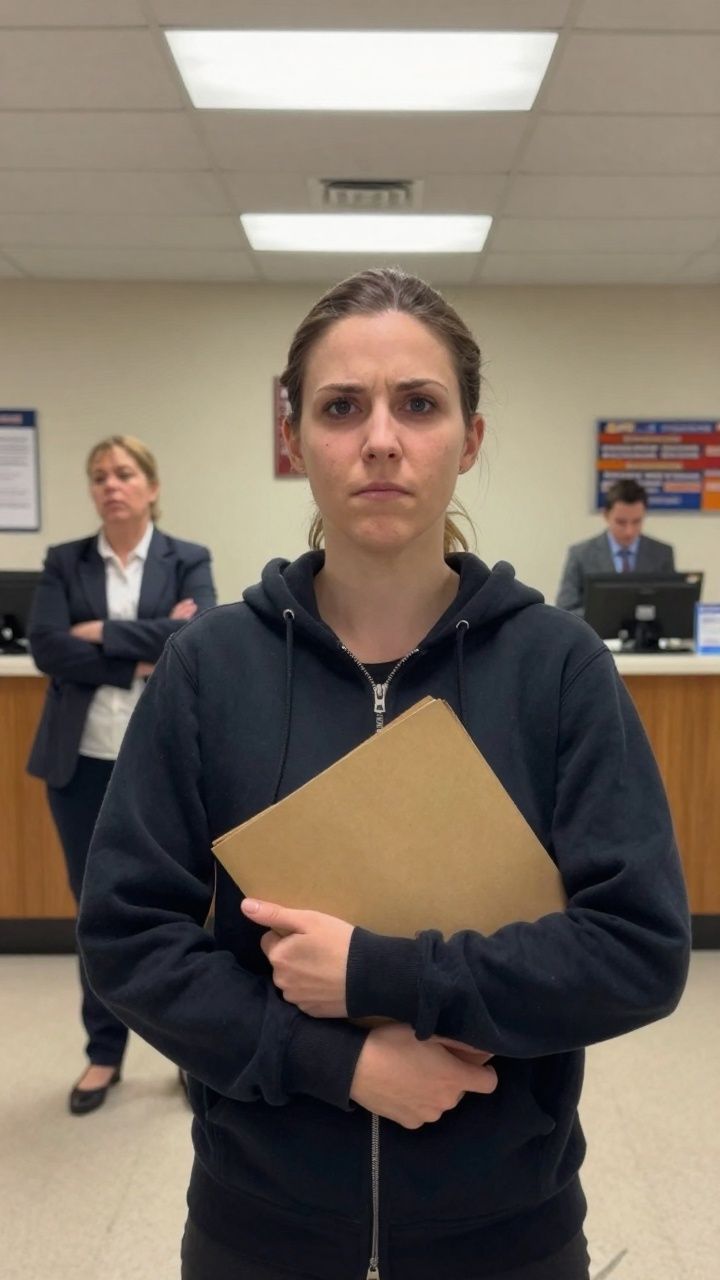

I want to be fair. I walked in calm. That part is true.

I’d rehearsed in the car. I knew what I was going to say and in what order. I was wearing my work blazer because I wanted to look like someone who kept receipts, which I am and I do.

Diane came out from her office after about seven minutes. She shook my hand with both of hers, the kind of handshake that’s supposed to communicate warmth but communicates the opposite. She had the smile of someone who’d taken a customer service training once and never forgot it.

I laid the folder on the little table in the side seating area and walked her through it. Transaction records. PT receipts. Timeline. The bank’s own elder financial exploitation policy, which I’d found on their website and printed in its entirety, fourteen pages.

She flipped through the pages without really reading them. I could tell. She’d flip to a new page before she could have finished the previous one.

When I finished, she folded her hands.

She said the transactions showed proper authorization. She said the bank had procedures. She said, and I am quoting this as close to exactly as I can, that sometimes elderly customers “make financial decisions that their family members don’t agree with” and later characterize those decisions differently.

I asked her to say plainly what she meant.

She said my mother may have “made decisions she later regretted.”

I’ve replayed those words probably two hundred times since then. Decisions she later regretted. As if Rosemary had impulse-bought a timeshare. As if the fourteen Tuesdays with Dennis the PT guy were something I’d made up. As if I hadn’t just put twelve appointment receipts on the table in front of her.

My hands went bloodless. I remember noticing that. Looking down at my hands and thinking, huh, that’s interesting.

The Lobby

I didn’t plan what happened next. I want to be clear about that, because some of my friends seem to think I walked in there with a speech prepared.

I didn’t.

I just didn’t leave.

Diane stood up, which I think was meant to signal that the meeting was over. I stayed sitting for a second. Then I stood up too. And instead of walking toward the door, I took three steps toward the middle of the lobby.

The branch wasn’t packed. Maybe eight customers. Four tellers behind the counter. A loan officer in a glass office to the left who’d been watching us through the window.

I started talking.

I said: this branch processed fourteen unauthorized wire transfers from a disabled 71-year-old woman’s account. I said the total was $47,000. I said I had documentation showing she was at physical therapy appointments during ten of those transactions. I said I had called the fraud line two weeks ago and heard nothing. I said the bank had a legal obligation to report elder financial exploitation and I had a printed copy of that policy in my hand if anyone wanted to read it.

I said Diane had just told me my mother chose this.

A woman in line turned around. Then the man behind her. One of the tellers — young, maybe 22, short hair — went very still.

Diane said, loudly, that I needed to lower my voice.

I said I wasn’t raising my voice. Which was true. I was speaking at a completely normal volume. The lobby had just gone quiet.

She said she would call security.

I said okay. And I kept talking.

I didn’t scream. I didn’t cry. I didn’t call anyone names. I just said the facts out loud in a room where people could hear them. The dollar amount. The dates. The woman who could barely walk. The fourteen Tuesdays.

The man near the back had his phone out. I noticed him. I thought he was recording. I didn’t care.

What Came After

Security came. He was a heavyset guy, maybe 55, named, according to his badge, Keith. Keith asked me very politely if I’d be willing to step outside. I said yes, actually, I was done.

I went to my car. I sat there for a minute. My hands were shaking by then, which they hadn’t been inside.

I drove home and called a lawyer I know from my husband’s work, a guy named Phil Dormer who does mostly real estate but knows enough to point me in the right direction. He told me to file a complaint with the state banking regulator that afternoon and also contact the Consumer Financial Protection Bureau. He gave me two more names.

I filed everything that night.

Three days later, I got a call from a woman at the bank’s corporate office. Not the branch. Corporate. She was careful and professional and said they were “taking the matter very seriously” and had launched an internal review.

Two days after that, Phil called me.

The man in the lobby with the phone wasn’t a customer. He was a reporter. Local news, investigative unit, doing a story on elder financial fraud in the state. He’d been at the branch that day following a different lead entirely.

He’d filmed the whole thing.

He called the branch for comment before his piece ran. That’s apparently when things moved fast.

Diane and one other employee — a teller whose name I still don’t know, the one who’d processed at least six of the fourteen transfers — were let go within the week. The bank hasn’t said anything public about why. They don’t have to. But Phil says the internal review found what I found: the transactions were processed without Rosemary present, and someone signed off on them anyway.

Whether that was negligence or something worse, I don’t know yet. That part’s still going.

The $47,000 is not back. That’s the part that keeps me up. Gerald is somewhere. The money is somewhere. The state’s financial crimes unit has a case number now, and an FBI field office has been in contact because the wires crossed state lines, and I’ve been told these things take time.

Rosemary doesn’t fully understand what happened. She knows Gerald wasn’t who he said he was. She cried once, on the phone, and then she didn’t bring it up again. She asked me last week if I thought she was stupid.

I told her no. I told her he called every Tuesday for months. He was patient and he was practiced and he knew exactly what he was doing.

She said, “Well. He had nice manners.”

That’s Rosemary.

I don’t know if I’m the asshole. I know what I did. I know why I did it. I know that two weeks of phone calls and fraud line reviews produced nothing, and forty minutes in that lobby produced an internal investigation, two terminations, and a reporter who put it on the local news.

Make of that what you will.

—

If you know someone with an elderly parent, send this to them. Not to scare them. Just so they know to check the wires.

For more wild family drama, read about a shoebox full of secrets or a letter from beyond the grave. And if you like a good confrontation, then you’ll love this story of an ex getting his comeuppance.